Finance

Latest in Finance

Discover the most recent articles in this category

2026-06-20 00:00:56.666 • by

Alex Ingram

Elon Musk became the world's first trillionaire after SpaceX's IPO, leading to widespread concern among Americans whose retirement savings are increasingly and involuntarily tied to the company and other AI firms through index funds, sparking fears of inequality and market instability.

2026-06-19 18:00:56.75 • by

Albert Inestein

Elon Musk's new trillionaire status, following SpaceX's $1.77tn IPO, has sparked widespread concern among Americans whose retirement savings are increasingly and involuntarily tied to tech and AI companies through index funds, raising fears about inequality and market instability.

2026-06-13 06:01:30.246 • by

Amanda Ireland

Elon Musk became the world's first trillionaire after SpaceX's IPO, but critics argue this valuation is based on hype, self-dealing, and regulatory capture, not economic fundamentals. The article warns that rule changes in major stock indices could force millions of Americans' retirement savings into this speculative venture, potentially leading to a significant wealth redistribution from ordinary investors to Musk and his associates.

2026-06-12 18:01:00.477 • by

Amanda Ireland

Elon Musk has become the world's first trillionaire after SpaceX's IPO, but critics argue his unprecedented wealth is built on hype, political connections, and arbitrary control, rather than sound economic principles, potentially rigging the financial system against ordinary investors.

2026-05-21 12:02:07.146 • by

Alex Ingram

Carrie Joy Grimes, author of 'The Joy of Money,' challenges common financial shame and 'crash diet' advice, offering practical tools and negotiation strategies to help individuals save money, manage debt, and navigate a challenging economy, emphasizing that financial empowerment is achievable for everyone.

2026-05-11 18:04:35.873 • by

Alex Ingram

Despite rising oil prices due to the ongoing war with Iran and consumer discouragement from high gasoline costs, the U.S. stock market continues its upward trend, with major indexes like the S&P 500, Dow, and Nasdaq inching towards new records, fueled by strong corporate profits and a resilient economy.

2026-04-30 12:01:30.586 • by

Alfred Ignacio

Jerome Powell announced he will remain on the Federal Reserve board after his term as chair ends, citing threats to the central bank's independence from Trump administration legal attacks. This decision could complicate incoming chair Kevin Warsh's plans for rate cuts and has drawn criticism from Trump, while the Fed itself faces internal divisions over future rate policy amidst a complex economic outlook.

2026-04-28 18:01:09.378 • by

Andrew Ismail

Wall Street's record rally ended abruptly on Tuesday, hit by slumping AI stocks amid concerns over OpenAI's spending and rising oil prices fueled by the Iran war. While major tech companies prepare to report earnings, some firms like Coca-Cola and JetBlue managed to post gains, offering a mixed picture for investors.

2026-04-10 12:01:20.496 • by

Alice Ibarra

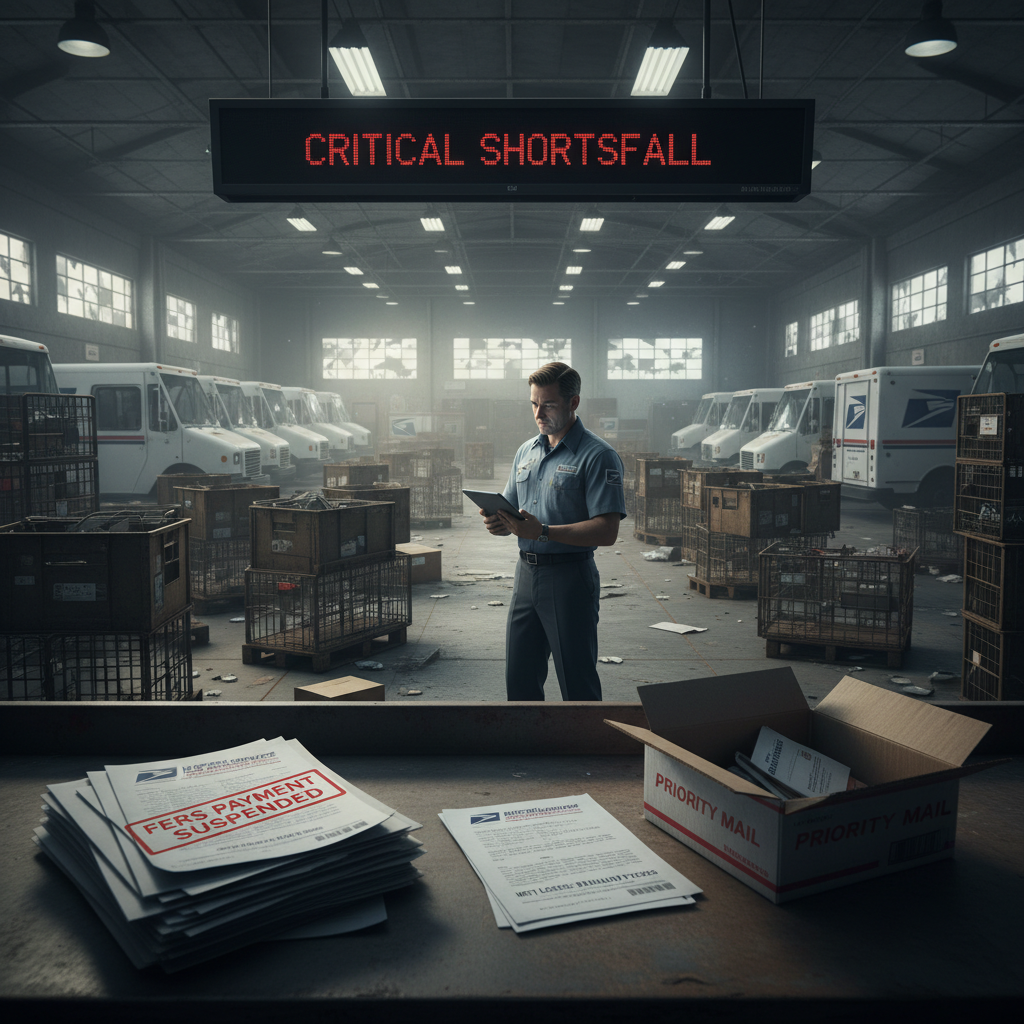

The U.S. Postal Service has temporarily suspended its employer contributions to federal employee retirement annuities (FERS) to address a severe liquidity crisis, ensuring it can continue payroll, pay suppliers, and deliver mail. While employee contributions, TSP, and Social Security payments will continue, and current/future retirees are not immediately impacted, the move highlights the USPS's dire financial state, exacerbated by declining mail volume and legislative constraints.

2026-04-10 06:01:38.963 • by

Aaron Irving

The U.S. Postal Service (USPS) has temporarily suspended employer contributions to federal retirement annuities to maintain liquidity, ensure payroll, and continue mail delivery amidst a severe financial crisis. While retirees are not immediately impacted, the move highlights deep-seated financial woes and calls for urgent congressional action on legislative reforms and borrowing limits.